Releases: Open-Lemma/options-implied-probability

Releases · Open-Lemma/options-implied-probability

OIPD v2.0.4

We made a no-code web interface!

- Check open-lemma.com

- And revamped the documentation to be much clearer

Thanks to our new contributors 👇 👇

A lot of bug fixes!

Probability Domain and CDF Improvements

- Added full-domain probability grids for

ProbCurveandProbSurface,

including smartgrid_points=Nonesizing and explicitfull_domain=True

exports/plots. - CDFs now use the 1st derivative of call-price instead of integrating

the PDF (which is itself a 2nd derivative) density_results()andplot()now default to compact, smooth view domains;

pointscontrols view resolution, whilegrid_pointscontrols native

numerical resolution.

Lazy Probability Materialization

- Added lazy probability materialization for

ProbCurveandProbSurface.

Probability objects store the fitted-volatility recipe first and

build price/PDF/CDF arrays only when queried, exported, or plotted. implied_distribution()now acceptsgrid_points=Noneand

cdf_violation_policy="warn".

Warning Diagnostics

- Added

warning_diagnosticsevents and summaries on public curve and surface

objects, with concise grouped warnings instead of repeated row/expiry noise. - Added warn-and-repair CDF monotonicity handling via

cdf_violation_policy="warn"; strict users can choose"raise". - Added diagnostics for stale quotes, price fallback, SVI butterfly risk,

skipped expiries, CDF repairs, and fan-chart skips.

Market Data, Forward Inference, and SVI Robustness

- Improved Black-76 put-call parity forward inference: nearest-ATM selection,

selected-subset outlier filtering, richer diagnostics, and no influence from

far-from-ATM pairs that merely pass validation. - Temporarily disabled the default bid/ask relative-spread gate; explicit

max_bid_ask_relative_spreadvalues still apply. - Added bid/ask-only ingestion, raw yfinance

spot handling, and lowercasevolumepreservation. - Fixed SVI weighting so reliable bid/ask spreads take precedence over volume,

with diagnostics for the chosen auxiliary weight source and fallback reason. - Simplified the public volatility/probability API by hiding legacy

Black-Scholes, Newton solver, and explicit dividend-input knobs; default fits

remain parity-forward Black-76.

OIPD v2.0.3

What's Changed

- Updated valuation_date and expiry date to accept timestamps, instead of just calendar dates

- This provides support for 0DTE options

Case study: spotting advanced knowledge trading 18min prior to Trump tweet

Trump announced a 90-day pause on most reciprocal tariffs on April 9, 2025. Reuters reports indications of advanced knowledge trading

- Trump announced tariffs at 1:18pm, moving the SPY price substantially

- we see abnormal implied distributions starting from 1pm, prior to his tweet

Notes:

- implied distributions of 0DTE April 9 2025 options

- 1m frequency SPY price downloaded using Alpaca free API

- free 1m options data from London Strategic

OIPD v2.0.2

Minor updates:

- Added DataFrame export methods for fitted results:

ProbCurve.density_results(domain=None, points=200)ProbSurface.density_results(domain=None, points=200, start=None, end=None, step_days=1)- extended

VolSurface.iv_results(domain=None, points=200, include_observed=True, start=None, end=None, step_days=1)

OIPD v2.0.1

OIPD v2: Overview of new capabilities

Previously in v1, OIPD generated the probability distribution of a future asset on a single future date.

OIPD has advanced in 2 directions:

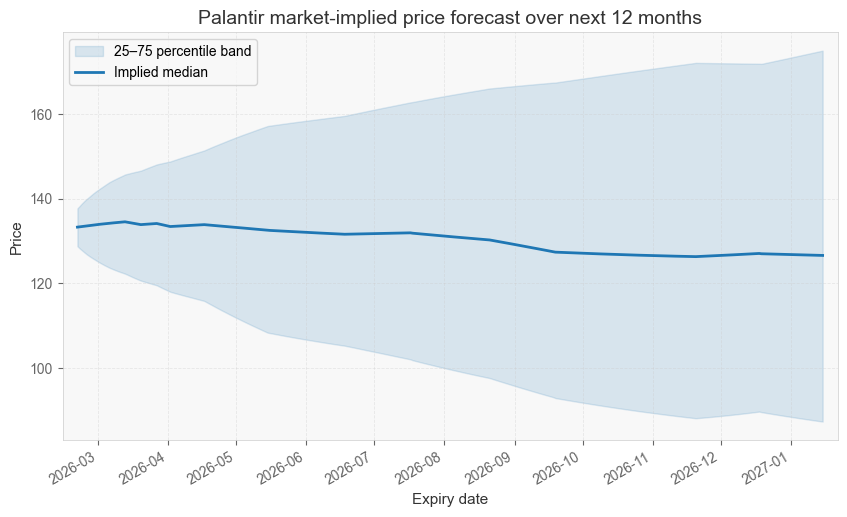

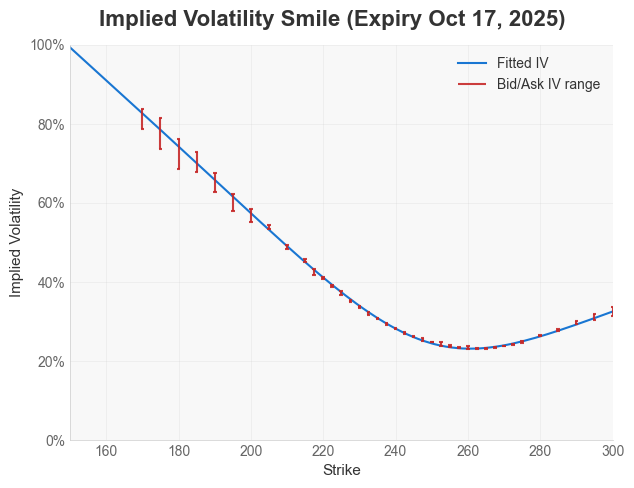

- It computes the market's expectations about the probable future prices of an asset, based on information contained in options data.

- It provides an opinionated, end-to-end volatility surface fitting pipeline:

v2.0.1 Updates:

- Improved the theory of interpolating the probability surface. Probabilities can't be interpolated over time directly, only the volatility smiles can be interpolated linearly in total-variance space. So we've made the

ProbSurfaceuse the fittedVolSurfaceto directly - Bug fixes: Made the

tinput consistent everywhere (same domain requirements and same type requirements)

Special thanks everyone who contributed to the development of v2:

Thanks to everyone who has contributed code:

And special thanks for support on theory, implementation, or advisory:

- integral-alpha.com

- Jannic H., Chun H. H., and Melanie C.

- and others who prefer to go unnamed

OIPD v2.0.0

OIPD v2: Overview of new capabilities

Previously in v1, OIPD generated the probability distribution of a future asset on a single future date.

OIPD has advanced in 2 directions:

- It computes the market's expectations about the probable future prices of an asset, based on information contained in options data.

- It provides an opinionated, end-to-end volatility surface fitting pipeline:

Special thanks everyone who contributed to the development of v2:

Thanks to everyone who has contributed code:

And special thanks for support on theory, implementation, or advisory:

- integral-alpha.com

- Jannic H., Chun H. H., and Melanie C.

- and others who prefer to go unnamed

1.0 release!

What's Changed

New Contributors

- @elainechang362 made their first contribution in #63

Full Changelog: v0.0.6...v1.0.1

Contributors

tyrneh and elainechang362